Two analyses examining long-term services and supports (LTSS) have been released recently, providing potential insights into payment and scalability for HCBS providers. The first is a Congressional white paper focused on long-term care insurance (LTCI), which is a policy designed to pay for extended care or LTSS required by a disability or chronic condition. The second is a new report from AARP’s Public Policy Institute, which focuses on the scalability of recent innovations. Here, we share highlights from each.

LTSS & LTCI

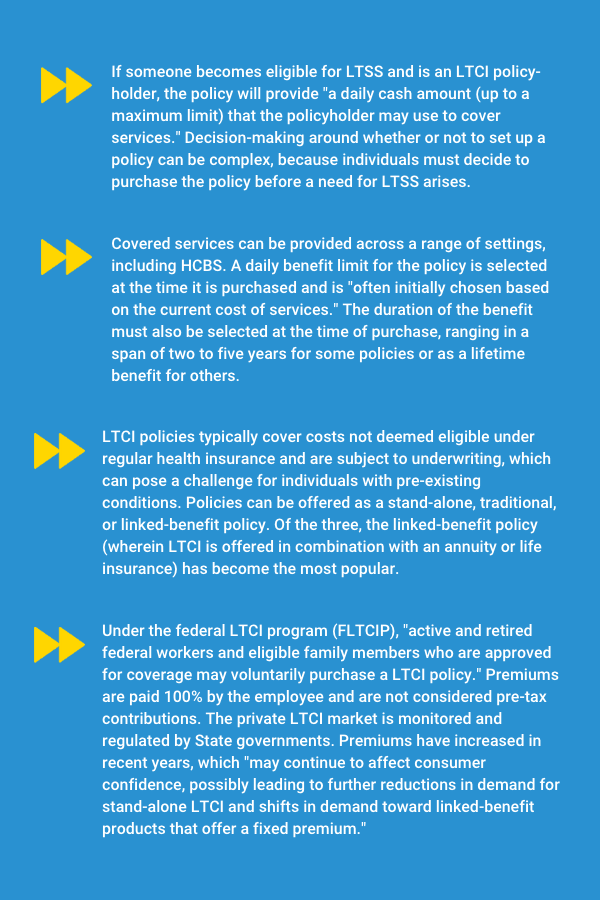

The Congressional Research Service (CRS) issued a focus white paper drafted by Kirsten J. Colello, a health and aging policy specialist, to provide an overview on LTCI. Topics covered in the paper included:

- A definition of LTCI;

- Policy features such as covered services, waiting periods and coverage amounts and length;

- Types of LTCI found in the insurance market; and

- Regulation, tax benefits, consumer protections and market stability.

LTSS: Scalability

The AARP Public Policy Institute released a new report on the viability of scaling recent innovations in LTSS, ultimately focusing on five that were deemed the most “promising.” The five innovations noted in the report were:

- Program of All-Inclusive Care for the Elderly (PACE)

PACE began in San Francisco’s Chinatown district in the 1970s and was designed to help “older adults of Chinese, Filipino, and Italian heritage live at home while receiving LTSS.” Currently, there are over 140 PACE sites serving an average of 470 people. - Green House® Nursing Homes

Started by Bill Thomas in the 1990s, the Eden Alternative combined a home-like environment with more activity choices and fewer psychotropics. This approach was integrated across New York state, and a grant from the Robert Wood Johnson Foundation funded Green House Replication Initiative to scale the model even further. Currently, there are over 370 trademarked homes situated on approximately 70 campuses across 32 states. - Self-Directed Home and Community-Based Services (HCBS)

HCBS programs, which provide beneficiaries with a monthly allowance to cover needed services, began in the 1960s. One of the very first examples was the Center for Independent Living, established in Berkeley to serve college students with disabilities.

“After successful testing of the “Cash and Counseling” program in the late 1990s and early 2000s, Medicaid, at the federal level, recognized two forms of self-direction: beneficiaries can employ workers directly, or they can manage a budget and purchase HCBS.” As of fiscal year 2018, nearly 4.8 million Medicaid beneficiaries received HCBS. - Supportive Services in Housing for Older Adults

In the late 1980s, this program was used by state and federal agencies to provide programs that would connect older adults with services in such a way that they could remain at home. Funding was provided in the late 1980s and early 1990s to expand the model, and in 2009 a Vermont nonprofit provider “piloted the SASH® (Support and Services at Home) model, which yielded increased positive results for residents while simultaneously reducing costs - Advancing Better Living for Elders (ABLE) and Community Aging in Place, Advancing Better Living for Elders (CAPABLE)

Johns Hopkins researchers initiated both the ABLE and CAPABLE programs, with the latter building upon the successes of the former. Both programs “rely on occupational therapy, physical therapy, and home repair professionals to improve LTSS for older adults and help them remain at home.” CAPABLE added a registered nurse and a handyperson to the list of potential visitors, and the program has shown consistent cost-savings.

Additional Reading

- To read the full CRS white paper, Long-Term Care Insurance: Overview, click here.

- To read the full AARP Public Policy Institute Report, From Ideation to Standard Practice: Scaling Innovations in Long-Term Services and Supports, click here.